Introduction

With enthusiasm, let's navigate through the intriguing topic related to Driving with a Shadow: Navigating Car Insurance for "Bad" Drivers. Let's weave interesting information and offer fresh perspectives to the readers.

Table of Content

Driving with a Shadow: Navigating Car Insurance for "Bad" Drivers

The open road beckons, promising freedom and adventure. But for some, the journey is fraught with a different kind of danger: the fear of sky-high insurance premiums. These are the "bad" drivers, those with a history of accidents, traffic violations, or even just a lack of experience, who face a daunting challenge when it comes to securing affordable car insurance.

This article delves into the world of car insurance for "bad" drivers, exploring the factors that influence their premiums, the strategies they can employ to mitigate costs, and the broader implications of this phenomenon on the insurance landscape.

The Price of Risk: How "Bad" Drivers Are Assessed

Car insurance companies are fundamentally in the business of managing risk. They assess the likelihood of a policyholder filing a claim based on a variety of factors, known as risk factors. These factors are then translated into a risk score, which ultimately determines the premium a driver pays.

For "bad" drivers, the risk score is higher, reflecting their increased likelihood of accidents and claims. The following factors contribute significantly to this higher score:

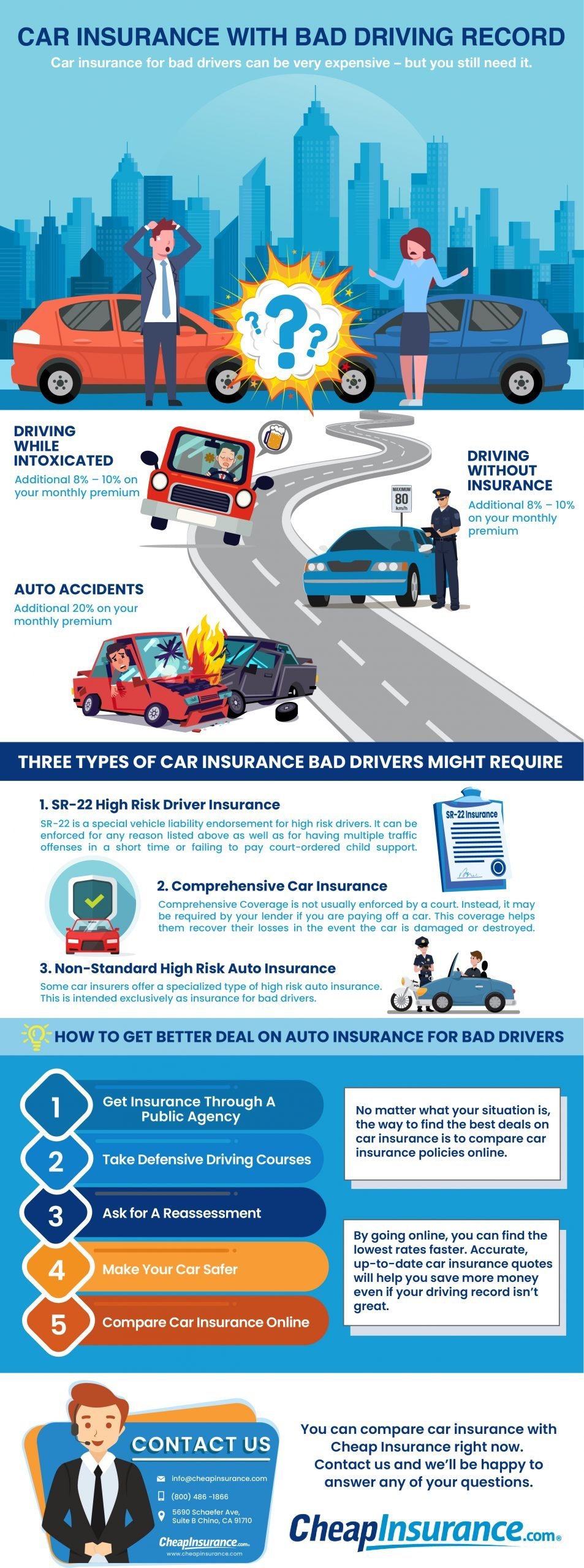

1. Driving History:

- Accidents: Even a single accident can dramatically increase premiums. Multiple accidents, especially those involving significant damage or injuries, can lead to a substantial price hike.

- Traffic Violations: Speeding tickets, reckless driving, DUI/DWI offenses, and other violations all signal a higher risk of future accidents.

- Driving Record: The length of time a driver has been licensed and their driving experience play a role. New drivers, with less experience, are typically considered riskier than seasoned drivers.

2. Demographics:

- Age: Younger drivers, particularly teenagers, are statistically more likely to be involved in accidents due to inexperience and risky behavior.

- Gender: While this factor is becoming less significant, historical data suggests that young men are more prone to accidents than young women.

- Location: Urban areas with high traffic density and congested roads tend to have higher accident rates, leading to higher premiums.

3. Vehicle Type:

- Performance Cars: Sports cars and other high-performance vehicles are often associated with reckless driving and higher accident rates, resulting in higher premiums.

- Vehicle Value: Expensive cars attract higher premiums due to the potential for greater repair costs or replacement value.

4. Personal Factors:

- Credit Score: In many states, insurance companies use credit scores as a proxy for risk assessment, with lower credit scores often indicating a higher risk of claims.

- Insurance History: Drivers who have a history of frequent claims or lapses in coverage may face higher premiums.

Table 1: Impact of Risk Factors on Car Insurance Premiums

| Risk Factor | Impact on Premium |

|---|---|

| Driving History | - Accident: Significant increase - Traffic Violation: Moderate increase |

| Demographics | - Age (young): High increase - Gender (male): Slight increase |

| Vehicle Type | - Performance Car: High increase - Expensive Car: Moderate increase |

| Personal Factors | - Low Credit Score: Moderate increase - Frequent Claims: Significant increase |

The High Cost of Being "Bad": A Case Study

Let's consider a hypothetical case study to illustrate the impact of risk factors on car insurance premiums. Imagine two drivers, both 25 years old, living in the same city, with a similar driving history. Driver A has a clean driving record, while Driver B has been involved in a minor accident and received a speeding ticket.

Figure 1: Hypothetical Car Insurance Premiums

| Driver | Driving History | Annual Premium |

|---|---|---|

| Driver A | Clean record | $1,200 |

| Driver B | Accident & Speeding Ticket | $1,800 |

In this scenario, Driver B's risk score is higher due to their less-than-perfect driving history. This translates into a 50% increase in their annual premium compared to Driver A.

Strategies for "Bad" Drivers: Navigating the Labyrinth

While the label of "bad" driver can feel like a burden, it doesn't have to be a financial death sentence. Here are some strategies that can help mitigate the cost of car insurance:

1. Improve Your Driving Record:

- Defensive Driving Courses: These courses can help drivers improve their skills and knowledge, potentially leading to discounts on insurance premiums.

- Avoid Traffic Violations: Even minor infractions can impact your insurance, so make a conscious effort to obey all traffic laws.

- Maintain a Safe Driving Record: Consistent safe driving practices will demonstrate to insurers that you are a lower risk.

2. Shop Around for Quotes:

- Comparison Websites: Utilize online comparison websites to gather quotes from multiple insurance companies.

- Direct Quotes: Contact insurance companies directly to obtain personalized quotes.

- Negotiate: Don't be afraid to negotiate with insurance companies to try and secure a better rate.

3. Consider Discounts and Bundling:

- Discounts: Explore potential discounts offered by insurers, such as good student discounts, safe driver discounts, or multi-car discounts.

- Bundling: Combine your car insurance with other insurance policies, such as home or renters insurance, to potentially qualify for bundled discounts.

4. Increase Your Deductible:

- Higher Deductible: Choosing a higher deductible can lower your premium, but you'll be responsible for paying more out of pocket if you need to file a claim.

- Weigh the Trade-Off: Consider your financial situation and risk tolerance when deciding on a deductible amount.

5. Explore Alternative Insurance Options:

- High-Risk Insurance Companies: Specialized insurers cater to drivers with less-than-perfect driving records, often offering coverage at higher premiums.

- State-Sponsored Programs: Some states offer insurance programs for high-risk drivers who have difficulty finding coverage in the traditional market.

The Broader Implications: A Ripple Effect

The challenges faced by "bad" drivers have broader implications for the car insurance industry and society as a whole:

1. Equity and Accessibility: The high cost of insurance for "bad" drivers can create an affordability gap, limiting their access to essential transportation. This can have significant consequences for individuals and communities, particularly those with lower incomes.

2. Risk Pooling and Premiums: The presence of high-risk drivers in the insurance pool can drive up premiums for everyone, as insurers need to account for the increased likelihood of claims.

3. Public Policy and Regulation: Governments are increasingly exploring policies and regulations to address the affordability of car insurance for high-risk drivers, such as expanding state-sponsored programs or promoting alternative insurance models.

Conclusion: A Path to Affordability and Safety

Navigating the world of car insurance as a "bad" driver can be challenging, but it's not insurmountable. By understanding the factors that influence premiums, exploring strategies to mitigate costs, and advocating for policies that promote affordability, individuals can find a path to affordable and safe transportation.

Ultimately, the goal is to create a system that balances the need to manage risk with the importance of providing access to essential insurance for all drivers, regardless of their driving history. By working together, insurance companies, policymakers, and individuals can strive for a future where the open road is truly accessible to everyone.

Related Articles:

- Navigating The Unfair: A Deep Dive Into Non-Fault Accidents

- Driving Into Uncertainty: Navigating Rental Car Reimbursement

- The Collision Coverage Conundrum: Demystifying A Vital Insurance Component

- The Local Advantage: Why Choosing A Local Car Insurance Agent Matters

- Navigating The SR-22: A Guide To High-Risk Car Insurance

Closure

Thus, we hope this article has provided valuable insights into Driving with a Shadow: Navigating Car Insurance for "Bad" Drivers. We appreciate your attention to our article. See you in our next article!

'Insurance' 카테고리의 다른 글

| Navigating The Unfair: A Deep Dive Into Non-Fault Accidents (0) | 2024.07.29 |

|---|---|

| The Safety Net: Understanding Liability Car Insurance (0) | 2024.07.29 |

| The Price You Pay For Peace Of Mind: A Deep Dive Into Car Insurance (0) | 2024.07.27 |

| Navigating The Maze: A Guide To Car Insurance Comparison Websites (0) | 2024.07.26 |

| The Price Of Freedom: Driving Without Car Insurance (1) | 2024.07.25 |